Auto Loan Calculator

Calculate payments over the life of your Loan

Home Blog Privacy Terms About ContactCalculate payments over the life of your Loan

Home Blog Privacy Terms About ContactPublished on October 12, 2025

My journey into the world of loan calculations started not with a big financial goal, but with a simple, nagging question. I was chatting with a friend about a home project, and they mentioned their loan had a surprisingly low monthly payment. I remember thinking, "How is that possible?" It seemed almost too good to be true, and that little seed of curiosity grew into a full-blown mission to understand the math behind the numbers.

I wasn't trying to make a big financial decision; I just wanted to feel less intimidated by the numbers. How could two loans for the same amount have such different payments? What was the hidden trade-off? I turned to the internet, armed with a handful of online loan calculators, ready to demystify the process for myself. My initial attempts were clumsy. I'd plug in a loan amount, an interest rate I saw in an ad, and a term, then stare at the monthly payment result. It felt like a magic trick, a number appearing out of nowhere.

But the magic was confusing. I could make the monthly payment number go up or down just by changing the loan term, the number of months. A longer term made the payment smaller, and a shorter term made it bigger. It felt counterintuitive. For a few hours, I was just sliding numbers around, completely missing the bigger picture. My focus was glued to that one single result: the monthly payment. I didn't yet realize that it was only one small chapter in a much larger story.

I want to be very clear from the start: this is my personal story about figuring out how these calculations work. It is purely for educational purposes and is not financial advice. My goal was simply to build my own literacy around these tools and the math that powers them, and I'm sharing what I learned along the way.

My real confusion began when I set up a specific scenario to test my understanding. I imagined a hypothetical project needing around $14,850. I found a representative interest rate online, say 7.8%, just to have a consistent number to work with. My goal was to see how the loan term—the length of time to repay—changed the calculation. This is where my narrow focus on the monthly payment led me astray.

First, I entered the numbers for a 60-month (5-year) term into a calculator.

Next, I tried a shorter term, 48 months (4 years), with the exact same loan amount and interest rate.

But that feeling didn't last. A little voice in my head kept asking, "It can't be that easy, can it?" If you're borrowing the same amount of money at the same interest rate, how can one option just be "cheaper"? I spent a good hour re-running these two scenarios, checking my inputs, and even trying a different calculator. The results were always the same. It was deeply frustrating. I felt like I was staring at a math problem where the answer was right in front of me, but I couldn't see how all the pieces connected. The monthly payment was a siren song, luring me toward an incomplete understanding of the real cost.

The breakthrough came when I forced myself to stop looking at just the monthly payment. I decided to meticulously examine every single field the loan calculator provided. I opened two browser windows side-by-side, one with the 60-month calculation and the other with the 48-month calculation. My eyes scanned past the bold monthly payment number and landed on two less prominent fields: "Total Interest Paid" and "Total Cost of Loan." Suddenly, the entire picture snapped into focus.

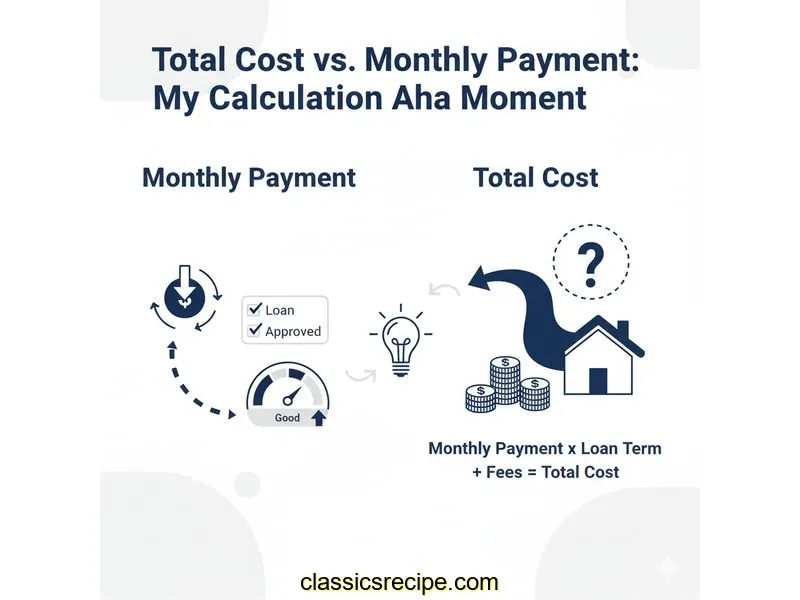

For the 60-month loan with the "cheaper" $298.61 payment, the total interest paid was $3,066.60. For the 48-month loan with the higher $361.38 payment, the total interest paid was only $2,496.24. It was a difference of over $570! The lower monthly payment came at the cost of paying significantly more in interest over the life of the loan. This was my "aha moment." The monthly payment is a measure of cash flow, but the total interest paid is the true measure of the cost of borrowing.

My new understanding wasn't just about one field; it was about how all the fields worked together. I learned that an interest rate is applied to the outstanding balance of the loan each payment period. In the beginning, the balance is high, so most of your payment goes toward interest. Only a small portion goes to reducing the principal (the actual money you borrowed).

This is where clicking that "Show Amortization Schedule" button changed everything. It generated a huge table with 60 rows for my first scenario. The first payment of $298.61 was split into roughly $96.56 for interest and only $202.05 for principal. But by the last payment, the split was reversed: only about $1.93 for interest and $296.68 for principal. A longer loan term means you spend more months in that initial, interest-heavy phase.

The 48-month schedule showed this even more clearly. Because the term was shorter, the principal was paid down faster. This meant there was less time for interest to accumulate on a high balance. The shorter term forced more of each payment to go toward principal earlier, which in turn reduced the total interest paid over the life of the loan. It wasn't magic; it was just math, working consistently over a defined period of time.

To make sure I really got it, I ran a completely different scenario. This time, I used a smaller loan amount, $8,200, and a lower interest rate, 6.5%. I compared a 36-month term to a 24-month term. Sure enough, the same principle held. The 36-month loan had a lower monthly payment, but the total interest paid was significantly higher than the 24-month option. This confirmed that my discovery wasn't a fluke of the specific numbers I'd chosen; it was a fundamental principle of how loan amortization is calculated.

After spending a weekend diving into these calculations, my entire perspective shifted. I went from being intimidated by the numbers to feeling empowered by my ability to understand them. Here are the key lessons about calculation literacy that I took away from this personal learning journey:

The simplest way is to use the results from a loan calculator. The formula is: Total Loan Cost = Monthly Payment x Number of Months (Loan Term). For my 60-month example, this was $298.61 x 60 = $17,916.60. To find the total interest, you then subtract the original loan amount: $17,916.60 - $14,850 = $3,066.60.

It's because interest is calculated on the outstanding balance periodically (usually monthly). With a longer term, your principal balance decreases more slowly. This means you have a higher balance for a greater number of months, leading to more interest being charged over the entire life of the loan.

While all fields are important, I found that the "Total Interest Paid" field gave me the most direct insight into the real cost. It isolates the amount you are paying just for the service of borrowing money, making it a powerful point of comparison between different loan scenarios.

An amortization schedule provides a transparent, payment-by-payment breakdown. It shows you the exact split between principal and interest for every single payment. By reviewing it, you can visually see how early payments are heavily weighted toward interest and how that balance shifts over time, which explains why total interest changes so much with the loan term.

My biggest takeaway from this whole experience is that understanding the story behind the numbers is incredibly empowering. I started out confused, focusing on a single number—the monthly payment—and ended up discovering how a handful of variables work together to tell a complete story. The loan calculator transformed from a magic box into a tool for learning and exploration.

I now see that the relationship between the loan term, monthly payment, and total interest isn't a trick; it's just a mathematical trade-off. Learning how that trade-off works has given me a new sense of confidence. I'd encourage anyone who feels intimidated by financial math to simply get curious. Pick a question, find a calculator, and start playing with the numbers. You might be surprised by your own "aha moment."

This article is about understanding calculations and using tools. For financial decisions, always consult a qualified financial professional.

Disclaimer: This article documents my personal journey learning about loan calculations and how to use financial calculators. This is educational content about understanding math and using tools—not financial advice. Actual loan terms, rates, and costs vary based on individual circumstances, creditworthiness, and lender policies. Calculator results are estimates for educational purposes. Always verify calculations with your lender and consult a qualified financial advisor before making any financial decisions.

About the Author: Written by Alex, someone who spent considerable time learning to understand personal finance calculations and use online financial tools effectively. I'm not a financial advisor, accountant, or loan officer—just someone passionate about financial literacy and helping others understand how the math works. This content is for educational purposes only.